![[Img #74664]](https://thelatestnews.world/wp-content/uploads/2024/12/James-Watson-The-controversial-genius-behind-the-double-helix-150x150.jpg)

To put the figures in context, during the last quarter of 2008, when the economic crisis that began in 2007 was already rampant, the drop was 36%.

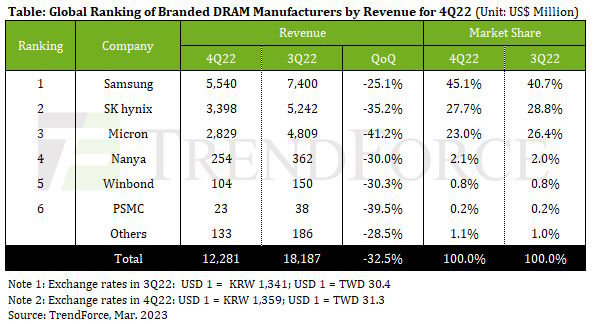

This loss of sales is going to have very harsh effects for manufacturers who are still facing a difficult situation after investing huge amounts of money to expand their production capacity before and during the pandemic, but who are now facing a slowdown in consumption and warehouses full of modules that cannot find a buyer.

All segments are affected, including professionals. TrendForce, in fact, points out that the DDR4 and DDR5 modules for servers registered quarterly drops in their negotiated price (contract prices) of 23~28% and 30~35%, respectively.

In general, all manufacturers are suffering, although some more than others. Micron, for example, is the most affected, with a quarterly decline in sales of just over 40%.

It remains to be seen what will finally happen during the first three months of 2023, but the situation is not rosy. Neither for the following quarters. Samsung, which usually takes advantage of crises to strengthen its facilities and get out of crises by stepping on the accelerator, plans to update one of its lines, which in turn should help move inventory by reducing product output. SK Hynix will also reduce its capacity in use, remaining at 92%, while Micron, which opted for a price reduction to lighten its stock, has dropped to 84% utilization.