It improves its deficit estimate to 3.3% of GDP, although it is still above the 3% estimated by the Government

June 11 () –

The Bank of Spain has raised its forecast for the growth of the Spanish Gross Domestic Product (GDP) by four tenths this year, from 1.9% to 2.3%, while it has maintained its estimates for 2025 and 2026, at 1. 9% and 1.7%, respectively.

The general director of Economy and Statistics of the Bank of Spain, Ángel Gavilán, explained, during the presentation of the new quarterly macroeconomic projections report prepared by the organization, that internal demand will be the main support of economic activity in the long term, especially , the private consumption component.

According to the estimates of the Bank of Spain, economic activity in the second quarter of the year will continue to show an appreciable rate of expansion, with GDP growth that could be around 0.5% quarter-on-quarter, somewhat lower than 0. 7% of the first quarter. This rate would be compatible with an interannual growth of the product in the second quarter of 2.4%, the same as that observed in the first.

Looking ahead to the coming quarters, the organization expects that GDP growth rates will gradually converge towards those in line with the potential growth capacity of the Spanish economy, which, according to estimates by the Bank of Spain, would be around 1. 6% year-on-year at the end of the projection horizon.

Among the factors that will act as support elements for GDP dynamism during the coming quarters, it is worth highlighting the gradual moderation of the negative impact on activity due to the accumulated tightening of financing conditions, the gradual reactivation of the European and global economy, the expected population growth, the increase in the real incomes of economic agents in a context of slowing inflation and the greater deployment of NGEU funds.

As a result of these developments, at the end of 2026 the GDP of the Spanish economy will be 8.9% above that registered before the start of the Covid-19 pandemic, an increase that, however, will be significantly lower (from 4.8%) in per capita terms.

Domestic demand will be the main support for activity and household consumption, which will be the component with the greatest positive contribution to GDP growth, will show increasing dynamism in the coming quarters. However, per capita consumption will not recover pre-pandemic levels until 2025.

For its part, gross fixed capital formation, which is still 2.2 points below its pre-pandemic records, will also increase throughout the projection horizon. However, it is warned that at the end of 2026, investment will be the component of demand that presents the lowest accumulated growth since 2019, which, with a longer time perspective, could hamper the dynamism of productivity and, therefore, the potential growth capacity of the Spanish economy for the future.

THE UNEMPLOYMENT RATE WILL CONTINUE ABOVE 11% IN 2026

Regarding the labor market, the Bank of Spain expects that job creation will continue over the coming years, although at a somewhat slower pace than that observed in recent quarters, so that there will be a certain recovery in productivity. .

The unemployment rate of the Spanish economy will still remain above 11% in 2026, although it will maintain a downward path, going from 11.6% in 2024, the same rate as the previous forecast, to 11.3% in 2025 – two tenths less– and 11.2% in 2026 –one tenth less–.

For its part, the agency has revised downwards its estimates for employment growth in 2024 from 1.8% to 1.1%, although it raises them in 2025 from 1.1% to 1.7% and the stands at 1.2% in 2026, up from 0.9% in the last report.

WORST OUTLOOK FOR PRICES THIS YEAR

Regarding the forecasts for general inflation, the Bank of Spain estimates that the CPI will be 3% in 2024, three tenths more than the previous forecast; at 2% in 2025, one tenth more, and 1.8% in 2026, another tenth more.

In any case, the organization points out that, in the coming quarters, the path of moderation in food inflation and core inflation will continue. Specifically, food inflation will decrease from an annual average of 11.1% in 2023 to 4.5% in 2024 and to rates around 2.5% in 2025 and 2026.

THE WITHDRAWAL OF VAT ON FOODS WILL PUSH UP PRICES

This evolution is consistent, among other aspects, with the prices observed in the futures markets for different food raw materials and with the marked deceleration that food prices have been showing in recent months in the initial stages of the production process. In any case, the slowdown in consumer food prices will show some ups and downs in the coming months.

Thus, for example, the reversal of the VAT reduction on food starting in July 2024 – if the Government decides not to extend this measure – will exert some upward pressure on these prices in the second half of the year, according to the agency has warned.

On the other hand, core inflation will decrease from an annual average of 4.1% in 2023 to 2.6% in 2024 and to rates close to 2% in 2025 and 2026.

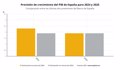

THE PROSPECTS FOR THE DEFICIT IMPROVE, BUT IT DOES NOT REACH 3% OF GDP

In its new projections, the Bank of Spain improves its estimates on the deficit for 2024 and places it at 3.3% of GDP, two tenths less than the previous projection, although three tenths higher than the Government’s projections ( 3%).

For 2025 and 2026, the organization cuts the deficit projection for 2025 by four tenths, to 3.1%, and places it at 3.2% in 2025 – compared to 3.5% in the previous forecast – which would leave Spain in a situation of non-compliance with the fiscal rules set by Brussels that requires lowering it below 3%.

UPWARD PATH OF DEBT BETWEEN 2024 AND 2026

Regarding the debt forecasts over GDP, the Bank of Spain’s estimates point towards an upward path between 2024 and 2026, despite the moderation observed in recent years since the peak caused by the pandemic.

Specifically, for 2024 the projections are 105.8%, better than the previous 106.5%; of 106.2% in 2025 (lower than 107.2% of the previous forecast) and 107.2% in 2026 (lower than 108.4% of the previous estimate).

RISKS: GEOPOLITICS, EUROPEAN FUNDS AND CONSOLIDATION PLAN

In any case, the Bank of Spain warns that these projections are subject to high uncertainty. In the external sphere, geopolitical tensions represent, in the event of an escalation, a considerable downward risk on activity and an upward risk on prices. Likewise, episodes of financial turbulence that cause a sharp correction in the prices of financial assets and a deterioration in the macroeconomic outlook in the short and medium term cannot be ruled out.

At the domestic level, there continues to be high uncertainty regarding the pace of execution of projects associated with the NGEU program and the savings capacity of households. There is also uncertainty about the persistence of the considerable dynamism in services, especially tourism, that Spain has maintained in recent quarters.

Furthermore, the implementation of a fiscal consolidation plan would foreseeably entail a lower degree of dynamism in activity throughout the projection horizon than that contemplated in this forecasting exercise.

Add Comment