Beijing’s Covid-zero policy and Russia’s war against Ukraine have hit the already struggling Chinese economy hard. Coping with this situation will come at a great cost in the long run.

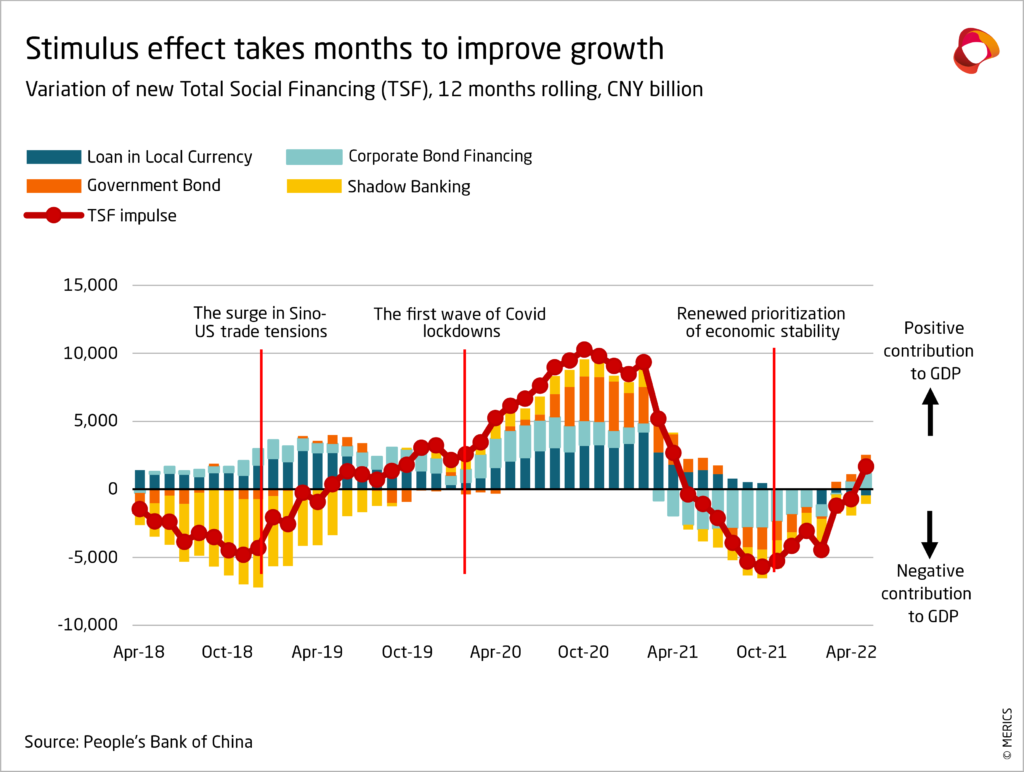

The Chinese economy is in a difficult situation, in a year in which social stability is at the top of the agenda as the Chinese Communist Party Congress (CCP), which takes place once every five years and will take place this fall. The restrictions on economic stimuli, which stem from the official mantra of “avoiding a flood of stimuli” and which have manifested themselves through defaults in the financial markets, have failed to produce a significant GDP growthwhich has forced Beijing to return to its old recipe of encouragement through construction. In doing so, it risks undoing hard-won reforms and useful changes in resource allocation.

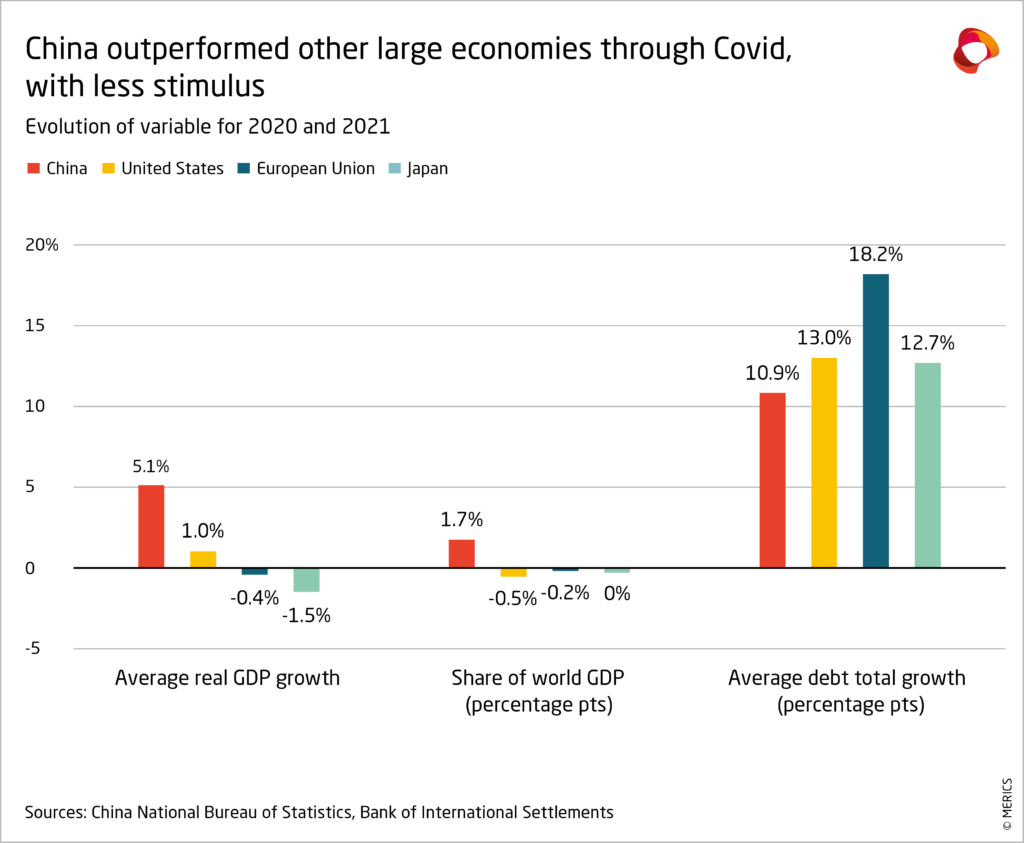

Recently, the lack of dynamism of the internal consumption has become apparent as the traditional growth engines of Beijing they lost momentum. China’s impressive economic performance during the coronavirus pandemic Covid-19 it overshadowed warnings about the sustainability of a dynamic driven mainly by exports and debt-financed investment. Subsequently, the decrease in foreign demand for digital products and the increase in the prices of raw materials moderated the first, while the tightening of regulation, focused on the real estate market and the digital economy, tamed the second.

Prices soar on war-induced disruptions

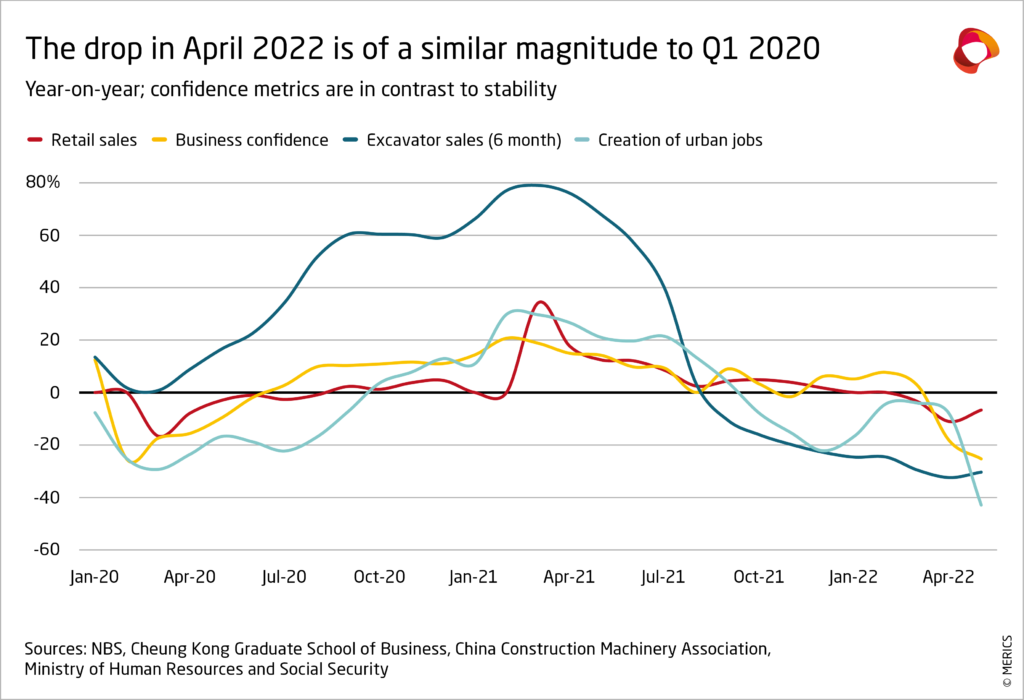

The Russian invasion of Ukraine and the rigorous zero covid policy from China added to the economic problems. As the world’s largest importer of most raw materials and agri-food products, China is seeing prices soar due to war-induced disruptions. Beijing’s geopolitical positioning and financial uncertainty led foreign capital that had been pouring in for 18 months to flow out again. And the back to lockdown they plummeted domestic demand, stagnant production and value chains. Mistrust spread the shock throughout the economy.

At first, Beijing seemed confident that he could still achieve his ambitious goal of GDP growth of 5.5% by 2022 by halting reforms and launching limited stimulus. The annual government plans, published in December, insisted on economic stability after a year of profound reforms. In fact, the regulatory tightening that had characterized 2021 was halted and interest rates were lowered. In addition, Beijing tolerated the first local measures of relaxation of real estate purchases.

Then Beijing felt the need to go a step further, with multiple measures to support production. The first Minister Li Keqiang acknowledged the dire situation in early April by making prices and employment the priority (implicitly abandoning this year’s growth target), while providing and asked for more support for the economy. He even arranged meetings ad hoc to tell the provincial authorities that they did everything necessary to prevent economic activity keep falling. Xi Jinping’s economic czar, Liu Hemade clear pro-market calls, while financial institutions seem to have mobilized to support financial markets.

But this was not yet flood of stimuli which Beijing had resorted to before, and the April lending data was very disappointing. They showed banks’ reluctance to lend to households and long-term loans to businesses, two areas explicitly prioritized by Beijing but very sensitive to economic sentiment. In addition, local governments did not apply for new bond issues as quickly as expected, defaults continued and real estate prices declined across the country. All this then led to a worrying rising unemployment.

Political objectives hampered a very responsive economy

The problem was not so much that the leadership of the CCP suddenly lost its economic touch, but rather that conflicting political goals were hampering an economy that is generally very responsive. Substantial reforms taking place since 2012 have introduced the market discipline, making it difficult for Beijing to direct growth in the short term: companies no longer benefit from the implicit guarantee of public bailouts if they are aligned with state interests; Real estate prices are no longer guaranteed to only increase; the ability of local governments to use debt-fueled financial resources to fuel local growth or support local champions has been constrained.

But the pressure of slowing growth revived once again the traditional Beijing trilemma: having to choose between the objectives of stable employment, better allocation of resources (ie structural reforms) and stable public debt. Since the stable employment is arguably the most important priority as the 20th CPC Congress, any ambitions for further structural reforms and steps towards debt sustainability have been shelved for the time being. As a result, Beijing is once again looking for a quick rebound in economic growth.

A return to old stimulus methods is likely

A return to the old methods of stimulation is likely to take place. One sign of this is that Li took advantage of an emergency meeting in late May with thousands of local groups to call for the unemployment rate to be lowered “as soon as possible.” As a result, local governments seem ready to get back to doing what they do best: rapidly securing economic stability and jobs through debt financed stimulus focused on construction and public bailouts of companies in difficulty. All recently announced measures point in that direction, while demand-side stimulus remains marginal at best.

Hard-won improvements in recent years to address the economic imbalances internal (rolling back old industries, increasing investment efficiency, tackling government and corporate debt) appear to be partially reversed. The reappearance of bad habits will delay the model of economic development preferred by the elites, based on technological innovation and economic efficiency. They will undoubtedly avoid a total collapse and buy time in Beijing. But with a rapidly aging population and a less favorable international environment, its economy will still have to quickly catch up to the productivity of advanced economies.

Article originally published in English in the Web of MERICS.

Add Comment