![[Img #74664]](https://thelatestnews.world/wp-content/uploads/2024/12/James-Watson-The-controversial-genius-behind-the-double-helix-150x150.jpg)

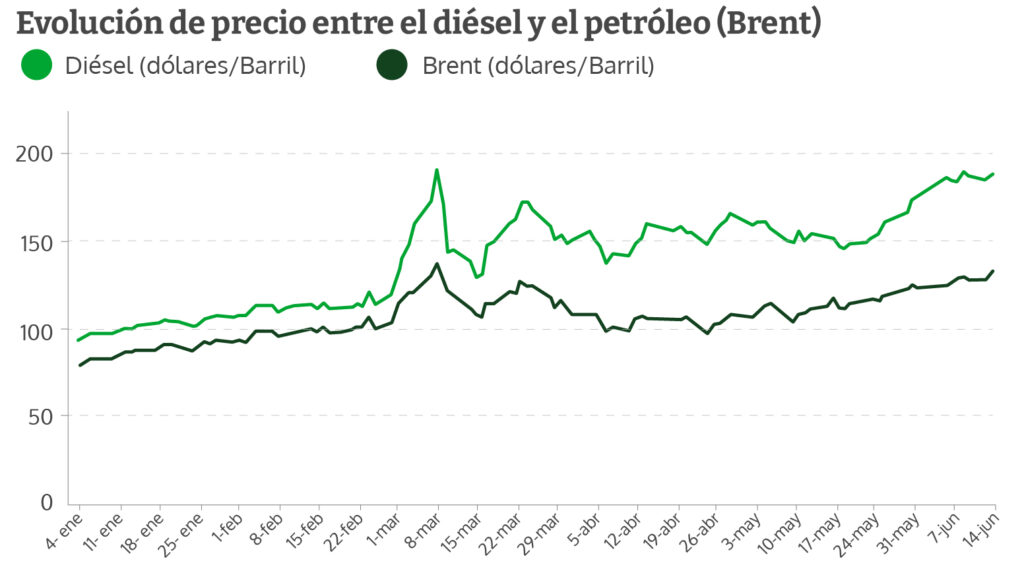

The blame for the high prices of the gasoline it does not have it only that the tap of the russian oil. A clear reflection of this is the increase in diesel, which represents 80% of fuel consumption in Spain. This derivative of Petroleum it has more than doubled the price of Brent crude, Europe’s benchmark, since the Ukraine invasion. A difference that resides in Europe has been forgotten in the last decade of the refining industry and is now paying for this neglect.

Europe is in full tension with Russia with a great weakness in the refining businessthe industry that is dedicated to converting oil into fuels such as gasoline, diesel, kerosene, propane, or butane. The European Union has closed 24 refineries, more than 10% of the continent’s refining capacity, since 2009. The main argument for this trend is the lack of profitability that European refineries were finding, despite the fact that the consumption of gasoline, diesel and kerosene has increased in the last decade by around 1.5%.

If a cut in supply from the main oil supplier, Russia, is added to this scenario of shortage of refining capacity, this industry blocks supply. As they explain from the sector to Vozpopuli, many European refiners are not ready to switch oil suppliers. Crude oil has different qualities depending on its origin and, depending on these properties, temperatures and a different adaptation of the distillation units are needed to achieve the desired fuels.

These factors have caused a lack of refining plants and that many of those that exist are only prepared for Russian oil. Therefore, they are left useless. There are cases like the German Stade refineryto the west of Hamburg, which is connected to an oil pipeline that comes from Russia, is one of the most relevant plants for supplying fuel in northern Germany.

Another famous case these weeks is the decision of the Austrian Government to release its strategic fuel reserves to avoid possible shortages after an accident at the country’s largest oil refinery. Austria has freed up 112,000 tons of diesel and 56,000 tons of gasoline to cover lost production due to an accident on Friday at the Schwechat refinery in Vienna.

It’s not just Russian oil

The problems in the oil refining plants adds to the cost of their operation. ANDThese plants are also affected by increases in electricity, the increase in the emissions market and the price of natural gas that they need for their operations. These deficiencies that the countries of the European Union have when it comes to converting oil into fuel in the last decade have also been compensated with the import of already refined product from their own partners.

The EU imports 18% of the diesel it consumes and, coincidentally, Russia is the main supplier. A difficult figure to replace because the possible candidate to replace this amount is China. Although, as the same sources in the sector warn, the Chinese government’s strategy is now to limit sales abroad to ensure its domestic supply.

Multiple factors that drive fuel prices out of control. Continuing with the specific example of diesel, until last June 15, the price of Brent crude had increased by 28% since the beginning of the Russian invasion to Ukraine, while diesel in Europe has skyrocketed in the same period by 66%. A fact that is especially sensitive in European inflation. Diesel is responsible for moving trucks, vans, excavators… Therefore, this fuel is one of those responsible for raising the cost of the entire supply chain of consumer goods in Europe.

What happens with refining in Spain?

The refining industry in Spain has gone in a completely different direction than in Europe. While the European Union has lost 10% of its refining capacity since 2009, Spain has increased its capacity by 16% since the same periodwith an investment of have invested more than €7 billion in this industry.

As described by the International Energy Agency (IEA in its acronym in English), “Spain has a large and relatively complex refining industry, with eight refineries to produce petroleum products.”. In addition, it has Asesa, a plant owned by Repsol and Cepsa, which from the sector is not included in the refinery group although it is responsible for producing asphalt bitumens, a key oil derivative in road construction.

Another refinery that is already left out of this list is located in Tenerife, owned by Cepsa. A plant that stopped distillation activities in 2018, but has served as a storage location to ensure uninterrupted supply to the Canary Islands. Repsol has five refineries (Bilbao-Petronor, Cartagena, La Coruña, Puertollano and Tarragona), Cepsa has two (Algeciras and Huelva) and British Petroleum (BP) It has its plant in Castellón.

The deployment of investments in Spain has allowed a greater adaptation to oil of different origins and that opens up the supply map more. Eight of the nine refineries are located on the coast and are easily supplied by ship. Only Repsol’s Puertollano refinery is in the interior and is supplied with crude oil through a 358-kilometre pipeline connected to the port and the Cartagena refinery.

These companies take advantage of their evolution with respect to Europe, although recognize that the national market suffers price stress due to the international factor that this industry has. Therefore, no matter how well things are done in a market, it will always ‘catch a cold’ if the European industry ‘sneezes’.

Refining companies do point out that Spain, thanks to the investment they have made in the last decade, not only has guaranteed security of supply for the population and industry. An argument that they will use in the coming months against the imminent tax that the Spanish Government intends to impose on the energy business.

Add Comment