![[Img #74065]](https://thelatestnews.world/wp-content/uploads/2024/10/Nobel-Prize-in-Physics-2024-150x150.jpg)

Even with all these factors against us, we always find funds that consistently achieve more than acceptable returns. It is the case of BNY Mellon Long-Term European Equity Fund. Although it is recently launched in UCITS, it is a strategy that has had its own track record since 1991, with the same management team, mainly Walter Scott.

In a very summary way, we could define the fund as large European companies focused on quality growth. The strategy is practically buy & hold with about 53 positions (the fund usually moves between 40 and 60) of which 21 have been in the portfolio for more than 10 years. Furthermore, the fund is Article 8 according to the SFDR regulation.

The system that Walter Scott has to analyze the companies that can become part of the portfolio is worth commenting on. It is true that each manager has a different approach, but Walter’s has some characteristics that I particularly like. Your analysis is based on 7 factors main.

- Valuation: valuation, capital, or liquidity metrics of the shares are analyzed. That is, not only if it is a cheap or expensive company in terms of PER, but a broader study is done.

- Company: the history of the company, its commercial activities, and the geographical and sector division are considered. This, which is usually done by all managers and analysts, is done here in a more complete way.

- Integrity: the focus is on risks and opportunities related to environmental, social and governance (ESG) factors, but analyzing integrity in all its aspects (much broader than traditional ESG) seems like a good idea to me. Integrity, a virtue that is conspicuous by its absence, seems to me to be key in the selection of securities.

- Market characteristics: the size of the company, its structure, long-term growth and the cyclicality of the sector in which it operates are reviewed.

- Control of destiny: Here the company’s power in its market, its market share, competitive advantage, pricing power and barriers to entry are examined.

- Financial profile: the long-term return structure, margin trends, cash generation and debt level, among others, are evaluated. The classic ratios.

- Management and Board: the experience of the management team, the track record of key executives, and the composition of the board of directors are valued.

I insist that it is no more special than other selection methods, but I particularly like it.

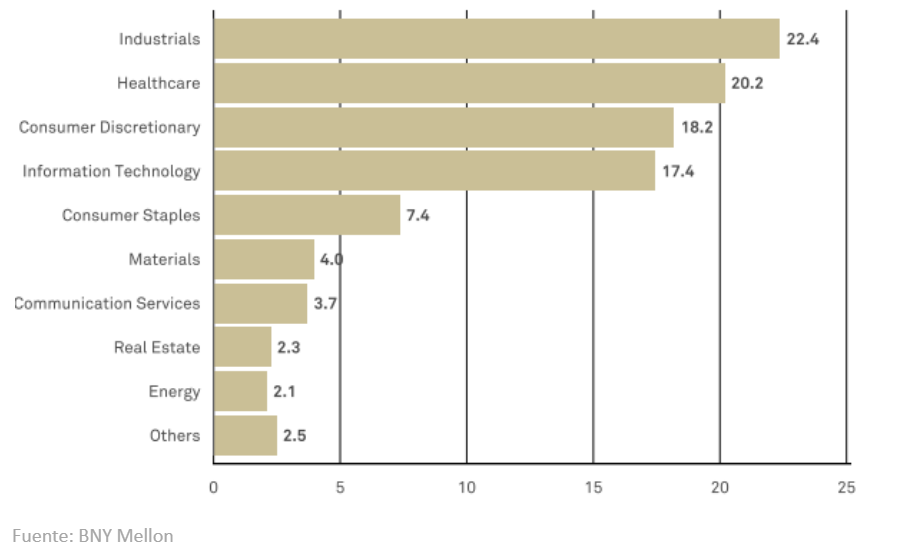

The main fund companies are well known: Novo Nordisk, SAP, ASML, Inditex, or Rocheamong others. and the composition by sectors I also like it for several reasons. The first of them is for the huge difference with an MCSI Europewhich gives it quite an advantage, given what we have said about our continent and how it lags behind. But it does focus on some sector of importance for Europe, such as the industrial sector, where there may be competitive advantages and on the few leading companies in technology. This mix of more traditional and faster-growing sectors is combined with a defensive and competitive advantage sector such as health. This arrangement of sectors seems very consistent to me. To add a “but” (a very personal opinion), discretionary consumption could be too high. Although it must be said that the companies in the fund that make up this sector are leaders and well known.

Another thing I like about the background is its country compositionwith greater weight in the United Kingdom, Switzerland, Germany, or the Netherlands, where country risks are lower and where the business environment is more favorable than in other parts of Europe.

The main ratios of the fund is not that they are exceptional, but they are if we measure it relative to the MSCI Europe Index. For example, a PE ratio of the fund of 28.5 is not exaggerated, but the European one is 14.7. That is to say, the potential of the companies in the portfolio, without being particularly expensive, is much greater than those in the index. The ROE is also much higher and the debt over equity is less than half.

And how does all this translate into profitability for the investor? Nice words and wise selection will have to lead to accompanying profitability. Indeed, in the long term, the The fund’s annualized return is 8.5%, almost doubling that of MSCI Europe. With greater volatility, yes, but almost doubling it. That “a picture is worth a thousand words” helps me close a brief explanation of a very unknown fund, but one that should be among the main European funds that we analysts look at.

Add Comment