![[Img #74664]](https://thelatestnews.world/wp-content/uploads/2024/12/James-Watson-The-controversial-genius-behind-the-double-helix-150x150.jpg)

The automotive sector has already been suffering in recent years. However, in 2024 the slowdown is becoming increasingly “dryer”. If we take into account the data from Spain, it is true that our country remains one of the ten largest automobile manufacturers worldwide, but it is also true that the volume of passenger cars leaving Spanish factories in 2023 was below 2.5 million for the fourth consecutive time.

Furthermore, if we stick to the most recent data, the idling is more noticeable. Spain, the car market fell by 6.5% in August (52,322 registered passenger cars) and, at the current rate, registrations will end the year below the million vehicle mark for the fifth consecutive year. With this outlook, the Spanish Association of Automobile and Truck Manufacturers (Anfac) has already revised downwards its forecast for the end of 2024, from one million to 980,000 cars.

Leading countries worldwide

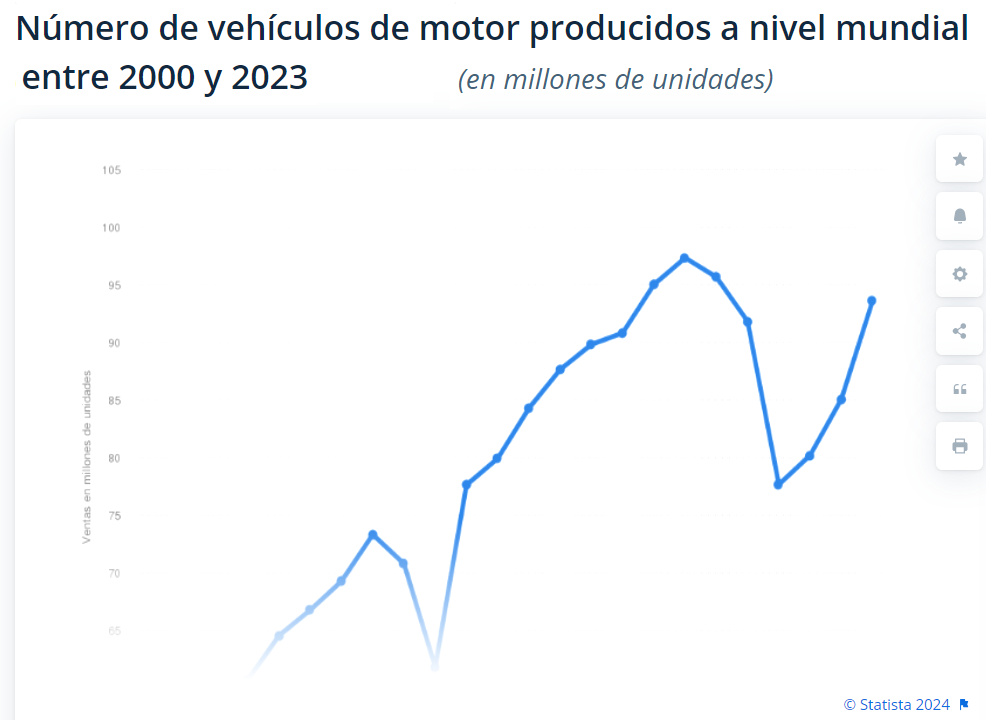

Globally, around 93.6 million motor vehicles were produced in 2023, an increase of 10% compared to the previous year and a figure that is very close to the values recorded between 2016 and 2018.

China led the world ranking of motor vehicles produced last year (with approximately 30.2 million), and did so by more than 19 million from the second largest car manufacturer, United States. Japanfor its part, completed the podium. Together, these three nations were responsible for more than half of global production of the sector, which is not surprising considering that some of the most relevant companies were born within its borders.

Germany and Spain were the two European countries in the ranking of the top ten producers in the global automotive sector, in sixth and eighth place respectively (France ranked 12th).

Warning signs in Europe

The automotive industry plays a major role in the European economy, employing 13.8 million people, contributing 8% of industry value added and boasting a trade surplus of €117 billion in 2023. However, this legacy is under threat. The sector is undergoing its most significant transformation in more than a century, driven by an emphasis on zero-emission vehicles, a shift in demand towards emerging markets and the integration of digital technologies.

In this sense, it is no secret that Demand for electric vehicles (EV) has continued to grow In the last decade, reaching a new high in 2023. Specifically, more than 14 million cars of this type were sold around the world, with a significant portion of them marketed in China. In fact, the Chinese company BYD is the leader when it comes to electric cars, with a market share of 21.1%, followed by Tesla which remained with 16.01%.

If we look at more recent data, between January and July of this year 2024 8.4 million electric vehicles have been sold, representing an increase of 21% compared to the same period in 2023, with China remaining the undisputed leader in this market, with 5 million units sold until July, representing an increase of 31% compared to the first 7 months of 2023.

In the same period, North American EV sales have also shown solid growth, although more moderate compared to the Asian country. Specifically, in the United States and Canada, one million electric vehicles have been sold by July 2024, an increase of 10%.

Emerging markets, while still small, are beginning to adopt electric vehicles at an accelerated pace, suggesting a shift in the global e-mobility landscape; their sales have grown 31% so far this year, although they still represent a smaller portion of the global market.

In contrast, the European market, which includes the European Union (EU), the European Free Trade Association (EFTA) and the United Kingdom, has shown signs of stagnation, with sales that have remained stable and without showing cumulative growth in the first seven months of this year compared to the same period in 2023. By country, while France and the United Kingdom have managed to increase their sales, with the French market growing by 6% so far this year, Germany has experienced a significant drop in its EV turnover, largely attributed to the end of the subsidies that had boosted the market in previous years.

Exits to an uncertain future

Bad data for Europe with a global market that is turning towards ecological mobility with EVs and software-defined cars. In this sense, it is estimated that By 2035, nearly 70% of total light vehicle sales will be electric cars. Furthermore, according to the ‘Electric Vehicle Outlook’ 2024, published by the International Energy Agency (IEA), almost one in five vehicles in the EU is expected to be electric by 2030, leading to a reduction in polluting emissions.

The slowdown in the adoption of electric cars, coupled with the rise of cheap electrified vehicles made by Chinese firms, is putting enormous pressure on the Old Continent’s automotive industry. This scenario could become even more complicated for Europe if it is not able to face other key challenges ranging from high production costs and fragmentation of the supply chain to rapid technological advances by global competitors, as well as a possible EU tariff policy on Chinese EVs.

In this regard, the recent EU report entitled “The Future of European Competitiveness”, led by Mario Draghi, analyses the current state of the automotive industry and outlines a comprehensive set of proposals needed to ensure that the region continues to maintain its competitive edge, through coordinated action on infrastructure, regulatory reform, competitive wage and energy costs, capacity development and innovation. According to Draghi, “a comprehensive approach is needed covering all phases” of automotive production, from research and extraction to data, manufacturing and recycling.

Volkswagen sounds the alarm and hits the European elite

But until that happens, the reality is that European carmakers are having a lot of trouble changing their combustion skin for an electric one, and the problems are already becoming noticeable at the business level. For the moment, Volkswagen It has only been the first (but not the last) affected. Just ten days ago, the German automotive group announced that it was not ruling out closing some of its factories in Germany, thereby forcibly laying off part of its team, in view of the need to reduce costs.

Similarly, Stellantis announced in June its plans to close its factories in Luton and Ellesmere Port, located in the United Kingdom, due to the unexpected slowness of demand for electric vehicles; the parent company of Citroën and Fiat warned that if the British government did not apply incentives to the purchase of electrified vehicles, it would close its facilities in both cities. For its part,Renault stopped production at its Flins-sur-Seine factory in March after 72 years of activity, beginning a conversion towards a “circular economy”; the end of the company’s vehicle production at this factory coincided with the announcement of failures in the production of the Zoé and Megane IV electric models.

On the other hand, the Swedish manufacturer VOLVO has abandoned its plan to sell 100% of its vehicles electrified by 2030. The company now expects electric and hybrid vehicles to account for 90%-100% of its total sales by the end of the decade.

This same week there was also bad news for the sector with BMWby admitting that 1.5 million vehicles will have to be recalled for their braking systems, which has led to a downward revision of its outlook for 2024. The reflection on the stock market? Double-digit falls in value, which negatively affected the entire European automotive sector.

Added to all this is another major problem for manufacturers in the form of multi-million euro fines if they do not meet the EU’s climate targets. Specifically, The industry could face fines of up to 15 billion euros If the sales of EVs set by Europe are not accelerated: by 2025, these companies must reduce their vehicle emissions from 116 to 94 grams/km.

Is it time to sell on the stock market?

For their part, the analysis houses have already reacted as well. The latest has been Berenberg, which expects the European auto sector to remain volatile amid slowing EV momentum, trade tensions with China and regulatory uncertainties. The broker cuts its 2024-26 OEM automotive operating profit outlook by about 10% on average. It also notes that while EU tariffs on Chinese imports offer “temporary relief”, they are “too low to have a significant impact on the evolution of European electric vehicle market share in the long term”.

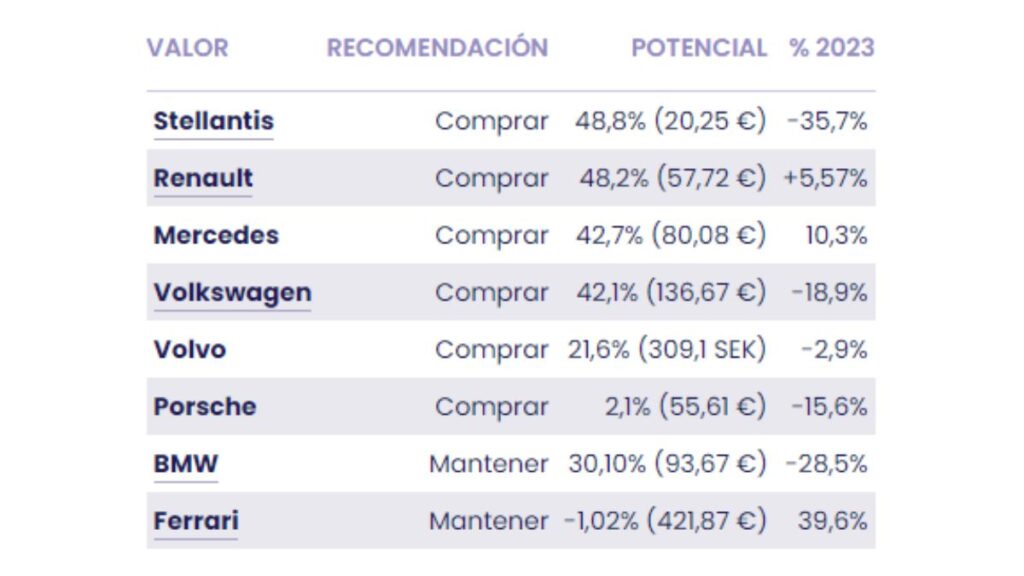

Does this mean investors should forget about the sector? Judging by what we can see in the Reuters consensus, it doesn’t seem like analysts think so:

Of the 8 leading stocks in the European sector, 6 have a buy recommendation and, of these, 5 also have double-digit potential in the medium term: Stellantis (48.8%), Renault (48.2%), Mercedes (42.7%), Volkswagen (42.1%) and Volvo (21.6%).

Add Comment