Aug. 30 () –

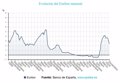

The Ibex 35 ended August with a revaluation of 3.04%, reaching 11,401.9 points – close to the annual highs reached at the beginning of June at 11,444 points -, driven by expectations of interest rate cuts, especially by the Federal Reserve (Fed), and the hope of a soft landing for economic activity.

According to market data consulted by Europa Press, the main indicator of the Spanish market has accumulated a revaluation of 12.87% so far this year.

Going into the details of August’s evolution, the month has shown two faces: on the one hand, the first week started with sharp falls – on ‘Black Monday’ on the 5th the indicator fell by 2.34%, its biggest drop since March 2023 – due to fear of a recession in the United States that spread to the Japanese Stock Exchange and, subsequently, to markets around the world.

On the other hand, after these initial setbacks, the month has been characterised by recovery and increases in prices that have led the Spanish index to flirt again with annual highs above the 11,400-point mark, to the point that, going into detail, the three weeks that make up the month have registered increases of 2.93%; 3% and 1.1% in this closing week.

On the other hand, it should be noted that trading volumes have been those typical of holiday periods and on rare occasions have more than 100 million shares traded per day been exceeded.

Market analyst Joaquín Robles explained to Europa Press that this rise in August was due to expectations of interest rate cuts and the hope of a soft landing, while inflation data in Europe and growth in the United States were better than expected.

Investors assume that, following the annual meeting of central banks in Jackson Hole in the middle of the month, the US Federal Reserve (Fed) will begin its monetary easing cycle in September with a first cut in interest rates (leaving them at 5-5.25%), while the European Central Bank (ECB) will make this move for the second time, leaving the reference rate at 4%.

Going into the details of the important macroeconomic references, he highlighted that the GDP of the United States in the second quarter of the year exceeded expectations and grew by 3%, dispelling fears of a rapid slowdown thanks to the pull of consumers, while this Friday it was published that the PCE inflation in July in that country remained unchanged at 2.5% and the underlying inflation stood at 2.6%.

In Europe, German and Spanish inflation rates were lower than expected in August (the former at 1.9% and the latter at 2.2%), which, according to Robles, puts “even more pressure on the ECB to cut rates for the second time this year.”

“The European body has many reasons to take action again, as while inflation is stabilising at the 2% target, in recent weeks there has also been a decrease in wage pressures and greater signs of economic weakness,” added the financial expert.

In the business sector, the main event was the publication of the results of the American technology company Nvidia, which exceeded expectations (it earned 168% more in the second quarter), but was affected by the cooling of its outlook for the coming year and its delays in the manufacture of a new chip.

In the national section, the evolution of Talgo has been particularly notable after the Government officially vetoed the proposal of the takeover bid of the Hungarian Magyar Vagón, although this entity has announced that it will appeal and has not ruled out launching another takeover bid in the future. The shares of the railway company, which are listed on the continuous market, have closed the week with a fall of more than 9%, to 3.89 euros.

For its part, IAG continues to register new annual highs after having announced this week an alliance with Royal Caribbean through its loyalty system, while the firm Brookfield would be looking for investors to join the takeover bid for Grifols.

In this context, within the Ibex 35, the monthly performance in August was notable for IAG (+10.37%); Inditex (+9.18%); Fluidra (+8.75%); Cellnex (+8.55%) and Grifols (+7.77%); at the other extreme, the worst monthly performance was for Rovi (-10.62%); Indra (-8.74%); (Repsol -5.46%) and Telefónica (-2.03%).

The bullish trend was the common denominator in Europe: London gained 0.12%, Paris 1.32%, Milan 1.8% and Frankfurt 2.15%. On the other side of the Atlantic, the Dow Jones and the S&P 500 advanced by more than 1%.

In other markets, oil remains subject to high volatility amid prospects of lower demand and tensions in the Middle East, with a barrel of Brent crude, the benchmark in Europe, falling 2.5% this month to $78.8, while Texas crude fell 3.7% to $74.

The troy ounce of gold rose by more than 2.3% in August, to $2,500, but on the 20th it reached a new all-time high of $2,531 amid the prospect of rate cuts. Bitcoin, on the other hand, fell by around 10%, to $58,300.

KEY POINTS FOR NEXT WEEK

Next week will be marked by employment data, which will be released at the end of the week, after the July figures contributed to the strong episode of volatility at the beginning of the month, so investors will take it as the most important reference before the first cut in September.

In this regard, Robles has said that “a bad figure could fuel speculation about a 50 basis point interest rate cut, although at the moment this seems unlikely.” The week will also be conditioned by benchmarks on manufacturing and services activity.

It should also be noted that the US market will be closed on Monday for the Labor Day holiday.

Add Comment